OUR ANGEL THE AUDITOR

Accountancy – Class 11 – Main Lesson

When that apocryphal villain of European folk tales, Bluebeard, was asked how many of his wives he had brutally dispatched to the hereafter, he replied, “What? I’m a murderer, not an accountant!”

The point here is that even relatively modest enterprises, like serial killers, need someone with accounting expertise to oversee their financial affairs. The Bluebeard tales are particularly astral in nature (blue is the nominal astral color!); describing a rampant ‘desire-body’ as they do. This supersensible organ of man is the dark heart of lust, bloodletting, obsessive wedlock and the like. Of course astrality has its noble side as well, as in a refined feeling life, artistic sensitivity, and so on.

In Anthroposophical physiognomy, we have a feature called the “accountant’s knoll”; this is on the top of the head, in the ‘astral’, the second quarter from the front, region – right on the top of the head actually. Common parlance calls accountants and their ilk ‘bean-heads’. This feature was identified particularly by cartoonists (like your author!) because so many “bean-counters” were endowed with it. Another gem of wisdom from the vernacular refers to figures folk as “pointy heads”!

One aspect of the astral world is the ‘number ether’; a supersensible realm one accesses when cogitating the numerical mysteries (as evidenced by Dustin Hoffman, the archetypal savant, in the film Rainman).

The astral sign of the four cardinal emblems of the Zodiac is Taurus; the bull expressing astral, or metabolic, power per excellence. Taurus was the (Northern Hemisphere) vernal sign in the Egypto-Chaldean-Babylonian (Han China in the East) era, from 2907 to 747BC. It was here, in both East and West, that the first records of accounting, or accurate commercial contracts, have been found. This is specially so in Ancient Babylon – “The whore (trader) who sits on the water” as this great center of commerce was uncharitably know. Trade was thought a necessary but lowly activity in days of yore; the province of negative astral types like scoundrels and swindlers! These commercial formalizations were thought to originate in Egypt, which extended its empire right up through Palestine, across the Tigris-Euphrates, and into Syria.

The Egypto-Chaldean partnership is exemplified in the person of Moses – a citizen of both worlds; his Chaldee name means “to be born”. Self-evident, yes? Until one realizes that names in the deep past carried cryptic codes; this particularly enigmatic appellation being connected with the mysteries of birth, a specific astral or ‘soul body’ revelation. Little Moses was, after all, the baby in the bulrushes!

To physiognomy again: Moses, Master of Weight and Measure, was sculpted by Michelangelo as having a pair of small horns. These are accurately positioned above the brow line on the third vertical band from the center of the head. This is yet another astral region, but frontal rather than profile.

Moses waxed strong in Pharaoh’s court with his weights and measures skills, and subsequently achieved wide responsibility for civil administration, especially the large, complex trading activities of the empire. As such, he would have had familiarity with, and perhaps was even an initiator of, modern profit-and-loss accounting procedures.

This seminal knowledge became the basis of the whole financial canon enshrined in the Cabbala, one which has sustained the Jewish people, via an inherited finance faculty, in relative prosperity for four millennia.

From this unlikely genesis, this Mosaic legacy, the Hebrews consequently became the paramount entrepreneurs and financiers right through the Western world – the Han Chinese (the “Jews of the Orient”, as they’re known) being their equivalent in the East.

In fact the first businessman in Judeo-Christian history is Noah. No, not as a boatbuilder, or stock transporter, but as a vintner. And a successful one too if his shameful inebriation (embarrassingly recorded in Genesis) is any indication!

Blass 11 is the best possible year in which to introduce young people to the labyrinthine (another bull-astral image) world of Accountancy, as this is the Taurus year in the 12-year unfolding of the Educational Zodiac (beginning Cancer in Class 1). Maths, with its Steiner-nominated Sense of Thought, is also the Taurus subject in the 12-fold Subject Zodiac – and that’s a lot of bull, er, bovine!

Accountancy is programmed as a main lesson, calling primarily on the head forces, on thought. Of the three maths main lesson strands, Accountancy is (obviously) slotted in the second, Finance. This evokes soul or feeling responses, so necessary as a counterpoint to the heavy cognitive emphasis inherent in the subject. Number without heart is a destructive force in soul life, as today’s ever-bloating economic rationalism attests.

The following is a colorful quote from a newspaper columnist fulminating about the profit smothering principle, greed over generosity, policies of our Federal government ‘money changers’ (I thought it might put a little sparkle into our otherwise dour subject, that’s all!);

“So damn them down in Canberra…a miserable clutch of bozo bottom liners, of scrimpers and scrooges, of fudging actuaries and fidgeting attorneys, a gaggle of thin-lipped (the physiognomic expression of meanness!) private school boys and yokel land grabbers and failed academics. Devoid of ideas and imagination, driven by pollsters and spin-doctoring leeches, dry as dust, stiff as sticks and cold as stone, they are a wretched crew with the spirit of ticket inspectors!”

Accountants rarely receive public applause or favorite press, their world being so arcane and inaccessible to mere mortals. They do however keep the wheels of commerce – and government – turning. Without their acumen, if not necessarily their good judgement, chaos would reign.

Even Jesus had an accountant, bookkeeper, business manager – whatever! Look how poor Judas has been savagely traduced over the centuries! This astral initiate was led into temptation – the astral invocation of the Lord’s Prayer – with his “30 pieces of silver” (the astral metal!).

These he cast away in contempt and remorse before he hung himself. This story is a timeless caution for humanity to separate matter from spirit – “Give unto Caesar what is Caesar’s, and unto God what is God’s” as Jesus so eloquently uttered as he held up a Roman coin – principle before profit is a modern interpretation.

One of the initiators of modern accounting and bookkeeping, the 16th Century Benedictine monk, Don Pieta, made a significant, spirit-inspired contribution to morality in business (his name means Mr. Good!). He asserted that a commercial enterprise was a separate entity – a Being indeed – from its owner/s. Rudolf Steiner honored this principle, keeping his modest financial affairs separate from those of Anthroposophy. The good Doctor has never been involved in a pecuniary scandal (or any other kind for that matter); all his Spirit of Contract dealings being beyond reproof. He owned almost nothing throughout his 64 years, and earned little. Conversely, the Movement he founded waxed strong, in time blossoming into a robust economic – not-profit – entity.

Alas, all has not been as ethically sound since his death, with many so-called ‘Steiner’ institutions corrupting, for the sake of filthy lucre, the most sacred of the principles he struggled so hard to midwife into the world. One example of this greed-based perfidy being the Steiner high schools which betray their founding fathers non-exam policy merely to attract government and other grants – Judases all! On this sad subject I could wax as lyrical as the disaffected columnist above!

But back to the history of Accountancy: The first evidence of double-entry bookkeeping was in Genoa in 1340; strangely synchronous with the birth of the Consciousness Soul, just half a century later. However the practical standard was so high at the time that it is presumed their methods – most still current today – originated much earlier.

Class 11 is also the 19th Century Year, that in which 17-year-old recapitulate Industrial Age consciousness. This included the shift, in 1879, of the globally reigned Zeitgeist from Gabriel to Michael – the age of a new, higher, ethic, financial and otherwise. Spiritual knowledge like this yet again assists in awakening in students a subliminal soul response. Formalized accounting procedures were born in the 19th Century.

Apart from the metaphysical imperative above, it is of great benefit to endow senior high school students, so soon to enter a world where accounting is such an integral part, with an overview of the industry. This includes a gladbag of fundamental financial skills with which to order their lives, both person and commercial. The accumulation of pecuniary faculties actually began four years earlier, in Class 8.

Here the Finance strand began with Personal Finance (see my book What is X? Why is Y?, Class 9 Small business; Class 10 Economics (both in Of Pine and Palm); and later in this book, Investment in Class 12.

An important segment in Accounting is qualifications and credentials; this kind of career information can be obtained from various organization, both private and public. A good idea also is a visit to a workplace, or invite a professional money-manager n to speak to the students. Here they will earn that the term bookkeeping is becoming redundant, as most accounts are managed on a computer.

In China, until relatively recently, calculations were done on that clever hand computer, the abacus. Actually Rudolf Steiner was scathing of this seemingly innocuous business aid; especially when related to the teaching of children. He referred to it as an instrument of materialism. What would he say about the omnipresent computer as a teaching-calculation aid?! This surely is Ahriman’s knock-out punch! There were of course commercial mechanical calculators extant in the good Doctor’s own time; though they were never permitted in his classrooms.

The economist or accountant rules supreme in today’s cargo-cult business world, but it was not always so. The bookkeepers being seen for what they really are, mere functionaries in the service of the soul or spirit of the particular enterprise – they are the body indeed. The Bible provides a no-hold-barred account of Christ’s displeasure with the ‘money changers’ – those who infested the holy precinct of the Temple at least.

This low regard for the finance-mongers is the main reason European Jewry was permitted to dominate the exchange industry, as their ‘betters’ considered it a demeaning vocation. “They’ve always done this kind of thing, let God – and His son – continue to revile them!”

In fact I was surprised when reflecting on this unit to recall that I was permitted – nay, privileged – to study Business Principles in high school – junior high at least. Surprised due to the fact that I was in one of the lowest classes. My own version of betters, the cream at the top of the educational milk jug smarties, rather studied languages, the sciences and the like. The faceless curriculum planners saw the future of my lowly ilk as toiling away over company books in some cramped, ill-lit back office; juggling the ink-smudged columns of profit-and-loss figures determined – for better or worse! – by front-office management policy.

Such was the status of business and bookkeeping education in the mid-1950s! In the many roles I’ve had since dealing with – if not usually wholly responsible for – company accounting, some of the basics I learnt in my Business Principles course have actually stood me in good stead.

For instance, I would impress my non-business principles colleagues by mysteriously knowing the difference between ‘accounts payable’ and ‘accounts receivable’ – or the more esoteric ‘bill of lading’ (particulars of goods shipped – lading meaning to load, or cargo).

Even the main three finance operative terms have their own hierarchy; an Economist determines economic policy; an Accountant supervises and audits the company records; while a Bookkeeper (or treasurer) makes the financial entries. These are done in ‘journals’ (daily entries – French ‘jour’, day), or ‘ledgers’, into which the debits and credits for the journals are entered, or ‘posted’.

A definition of Accountancy might be a good place to launch the content, both numerical and practical, of this important 3-week unit. The principles of accounting denote certain theories, behavioral assumptions, measurement rules and procedures for collecting and reporting information concerning the financial activities and objectives of a business entity.

Not only businesses, but almost every individual needs accounting skills, if even only to make a rough budget for daily needs. The imperative for increased skills comes when one has to run the finances of a family, small business, club; government department; or corporation.

Budgeting is the basis of accounting (‘to account for’); this is easy with regular income and regular expenses. It is the unpredictable which cause the problems, and all kinds of contingencies have to be considered. Budgets are made on a weekly, monthly, semester or annual, or even multi-year basis. The twin fundamentals of a budget are Income (regular and irregular and Expenditure (essential, non-essential and savings).

All budgets require to be regularly revisited to fit changing life circumstances. The one unchanging law of financial transactions is, like all other theaters of life, change. The budget also includes creditors, debtors, assets, depreciation, appreciation, and equity. The task of the budget is to keep the family, club, or company solvent (‘to solve’, as in problem). And to prevent insolvency, in the worst case, bankruptcy.

Interest and inflation are constantly eroding wealth, and the accountant must counteract this. Decisions on maintaining or increasing wealth by use of savings are based on Security, Interest and Notice.

The students should revise – if they’ve done it at all! – interest calculation. This knowledge can save fortunes over a lifetime, even for private individuals. For instance, what is the total amount payable on a loan of $25,500 on 12% over four year? First Reducible Interest.

Year 1 – $25000 = 12 over 100 X 25000 over 1 = 3060 + 6375 = $9435. Year 2 – $19125 = 12 over 100 X 19125 over 1 = 2295+ 6375 = $8670. Year 3 – 12 over 100 X 12750 over 1 = 1530 + 6375 = $7905. Year 4 = $6375 = 12 over 100 X 6375 over 1 = 765 + 6375 = $7140. Total Paid $33150 – Interest paid $7650. Now the same figures for Flat Interest: $25000 = 12 over 100 X 25000 over 1 = 3060 X 4 -= $12240 interest paid. Total repaid $37740. This is $4590 more than reducible interest – a fact business managers should be aware of!

Most businesses use check accounts, both for convenience and for accurate record keeping; they rarely resort to cash. No interest is usually paid on the balance of a check account, and there are also a range of bank charges for its use. The drawer is the person writing the check, the drawee the bank, and the payee the person to whom it is written.

A cash check can be cased anywhere; even one with a name on it can be; but one with a name which is crossed and marked Not Negotiable must be deposited into the payee’s bank account. The bank checkprovides safety with convenience – unless from some obscure overseas bank. Check information is kept o check butts, and the amount must be accurate – to the cent! – as these have to be reconciled against bank statements. I’ve seen a company accountant search the books for hours looking for a five-cent discrepancy so that her books would balance.

Of course there is always the problem that some of the checks haven’t been cashed, or the statement date is passed. Also bank charges, tax and the like do not appear on check butts. Accountants must regularly reconcile to establish the true state of the company finances at a given time. They must also be aware of the trends in the business; for this a profit and loss record is kept for the given year and several previous.

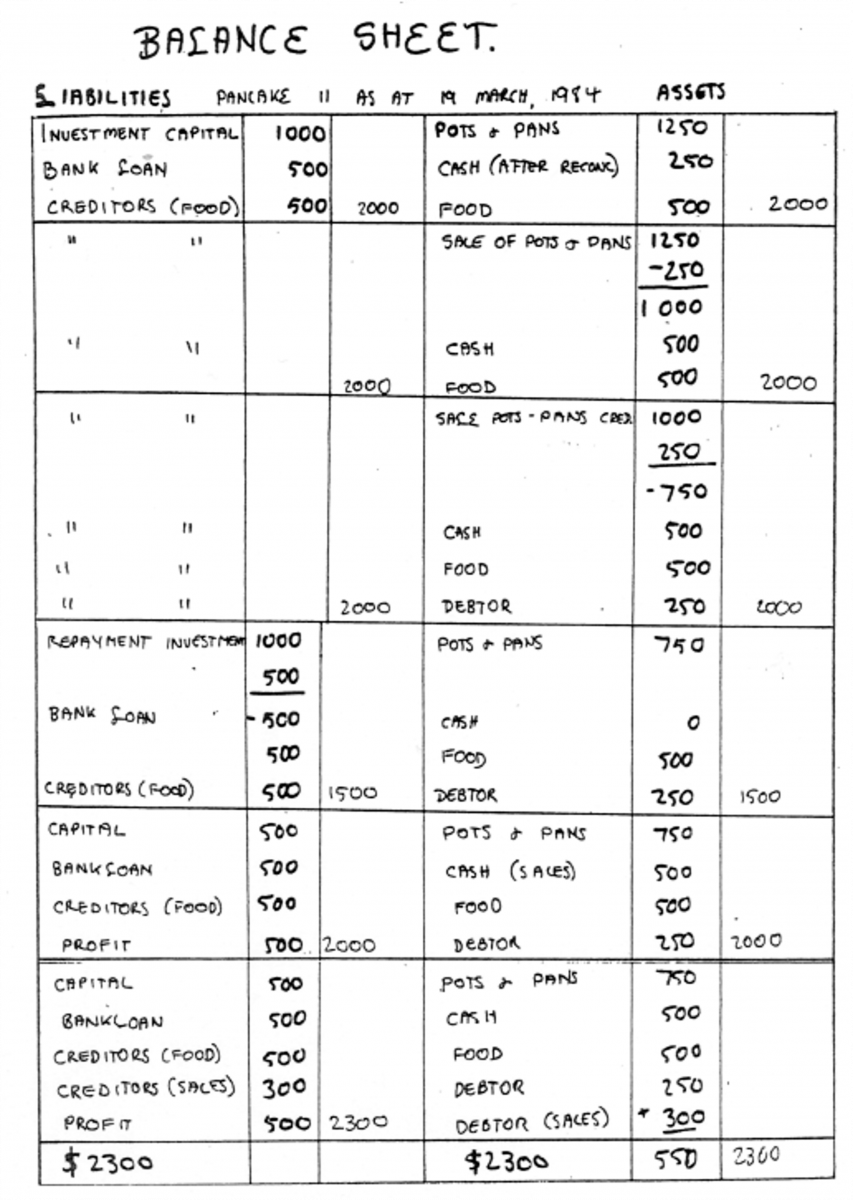

All companies begin with capital investment, a registered business name and a bank account. A double entry balance sheet is drawn up from the first day of trading. The liabilities column contains investments; loans owed; creditors; profit owed. The assets column includes material possessions; debtors; sales (assets and product); liquidity (cash); stock-in trade. The balance sheet is totaled after a set accounting period.

Another useful calculation is the Unitary Method: this is used to find the original sum if both the residue sum and its percentage is known. For example; if 7% of an original sum is $200, what is the original sum?

$200 divided by 7X100 = $2857.

Every public company must have its total financial transactions audited by a registered accountant. This audit has to be submitted to the appropriate authority, and is then after the Annual General Meeting, open for public scrutiny. At the AGM, the members of shareholders accept or reject the audited accounts.

The audit of a company is 12-fold, suggesting a sacred zodiacal principle =- I don’t think!! It is sent to all members prior to the AGM, and contains: 1. Notice of meeting. 2. Index of information. 3. Chairman’s report. 4. Index to schedules. 5. Auditor’s report. 6. Balance sheet. 7. Statement of general income and expenditure. 8. Statement of income and expenditure. 9. Directors’ statement. 10. Statement of source and application of funds. 11. Proxy forms. 12. Nomination form.

There are basically two kinds of companies, private and public. The latter are responsible to the public, and made up of shareholders or members. Private companies are responsible only to the owners.

The affairs of public companies are under greater scrutiny than private because they’re dealing with other people’s money. They must conduct the business along carefully prescribed lines, and have clear goals. These are stated in the company’s Memorandum and Articles of Association. His document, when approved by the authorities, becomes law, subject to even higher laws, like state or federal – higher still, if we consider the Laws of Establishment, under the regency of the Thrones, Spirits of Power!

The Memorandum contains the objects of the company; its goals are contained in sections and paragraphs. Memorandum s from ‘memory’, it is a reminder of why the company was originally created. The Articles rather ‘articulate’ the rules that the company agrees to abide by, these contain:

Preliminary; membership; admission of members; cessation of membership; rights of members; general meetings; proceedings at general meetings; register of members; subscribers; council; officers; secretary; representatives of members on council; vacation of office; casual vacancies; sub-committees; defect in appointments; alternate council members; meetings; minutes; declaration of interest; powers; sale of property; company seal; accounts; audit; indemnity; winding up; notices.

But back to some handy calculation: How much is a new wage if the old is increased by a certain percentage? A part-time worker on $224 receives a rise of 12%. 12% of $224 = 12 over 100 X 224 over 1 = $26.88. Therefore new wage is $224 + $26.88 = $250.88.

Before the balance sheet is presented to the AGM, a Trial Balance is drawn up. This is taken from the Trading Account, then transferred to the Profit and Loss account. The source documents begin with the invoice, evidence of goods received. The evidence of payment is the check butt or receipt. All transactions are recorded in the journal, which is in four sections: 1. Purchase on credit. 2. Sales on credit. 3. Cash receipts. 4. Cash payments. These are later transferred to a ledger containing columns with all major entries, like electricity, donations, etc.

There are two other sets of figures an accountant keeps an eye on, the Profitability Analysis and the Financial Stability Analysis.

A good accountant keeps a keen eye on these two calculations, if w/he is to prevent the company going bottom up! Profitability is assessed by four rations: 1. Gross Profit Ratio = Gross profit over sale; our example being $35500 over 71000 = 0.5 : 1 = 50%, or 50c in the dollar. 2. Net Profit Ratio = Net profit over sales = 16000 over 11000 = .022 : 1 = 22%, 22 cents in the $. 3. Selling Expense Ratio = Selling expense over sales = 3500 over 71000 = 0.05 : 5% : 1 = 50%, 50 cents in $.

The Financial Stability Analysis has two calculations. 1. Working Capital Ratio = Current assets over current liabilities = 9000 over 3000 = 3 : 1 = 300%, $3 in the $. 2. Property Capital Ratio = Equity over total assets = 32000 over 44000 = 0.72 : 1 = 72%, 72 cents in the $.

The unseen hand of the Thrones manifest itself to me many years ago in our school’s ABM. A scurrilous takeover bid by a group of parents (gullible) and friends (in sheep’s clothing!) used our voluntary treasurer’s somewhat imperfect financial accounts to impugn the credibility of the whole (again voluntary)_ School council, of which I was the Chairman. They savagely described her books as comparable to a local chook farmer!

Just as the vote was about to be taken, and control of the school lost forever to its initiators, a moment in which in enraged despair I’d hurled their perfidious submission to the floor, an eerie “thump – thump – thump” was heard in the corridor!?

It was the school’s – somewhat unpunctual! – accountant; he who audited and approved the said ‘chook farmer’ books. His name was Max Ruddock, our local state member of parliament, and father of Phillip Ruddock, currently Federal Minister for Immigration. The thumping sound was due to Max being burdened by a club foot!

When apprised of the situation, all our seething accountant said, in a menacing, varnish-melting tone, was that if another word was uttered which could be conceived of as critical of his audit, a $100000 (a fortune in 1973!) law suit for defamation would be on their desk first thing in the morning. The opposition, led and informed by an eminent Sydney Queen’s Counsel, capitulated immediately and absolutely.

Old Max, our esteemed auditor (previously thought of as a tiresome if necessary functionary) was indeed an angel in disguise – perhaps even a club-footed emissary of Their Exalted Selves, the Thrones.

An ancient depiction of the Thrones

Balance sheet for a Class 11 student’s imaginary company, from her Accountancy main lesson book.

Students are expected to create high-quality main lesson books for every subject, even Accountancy. This includes designing a beautiful or interesting cover. For this, my daughter Aanya used a found cartoon as a central element. Around this she wove a – very – short story:

THE TALE OF POOR WILLARD

Willard was born rich. When he grew up he inherited a $5,000, 000 estate. But Willard was foolish; instead of investing his money properly, he spent it on wine and women.

Willard was born rich. When he grew up he inherited a $5,000, 000 estate. But Willard was foolish; instead of investing his money properly, he spent it on wine and women.

But soon the bills started rolling in, and poor Willard started to realize his predicament. But it was too late, his estate was doomed!

“It doesn’t do you any good to site in the hot tub, Willard, if you sit in the hot tub and worry.”

Alas, due to his insolvency, poor Willard became a nervous wreck.

Then a wise prophet suggested to him “Why don’t you do an Accountancy course?” So Willard did, now read on…

And on the back page of the book:

And on the back page of the book:

After Willard did his Accountancy course, he decided that it wasn’t worth worrying about what was left of his estate.

So he gave it away, bought himself a motorbike, and went to work in a sock factory. The End.

As you can see, we don’t breed materialists in Steiner Education!

The Class 11 author of the above dares the reader to say her Accountancy book embellishments are out of character with the solemn nature of the subject.

Leave a Reply